The Psychology of Viral Content: How to Market Your Mortgage Expertise Effectively

Introduction

Mastering Mortgage Marketing Through Homebuyer Psychology is the essential key to elevating your business beyond mere transactions. Most online mortgage content is a "Glossary Trap." It gives clear definitions of technical terms, yet it ignores the anxiety and hopes that actually drive big financial decisions. This guide shifts the focus from simple definitions to the psychology of the homebuying experience. We will look at why homeowners feel overwhelmed, and we will also show how to use your skills to guide them through the complex and emotional world of modern finance. By viewing the homebuying journey as an emotional milestone rather than a technical hurdle, you position yourself as an indispensable partner.

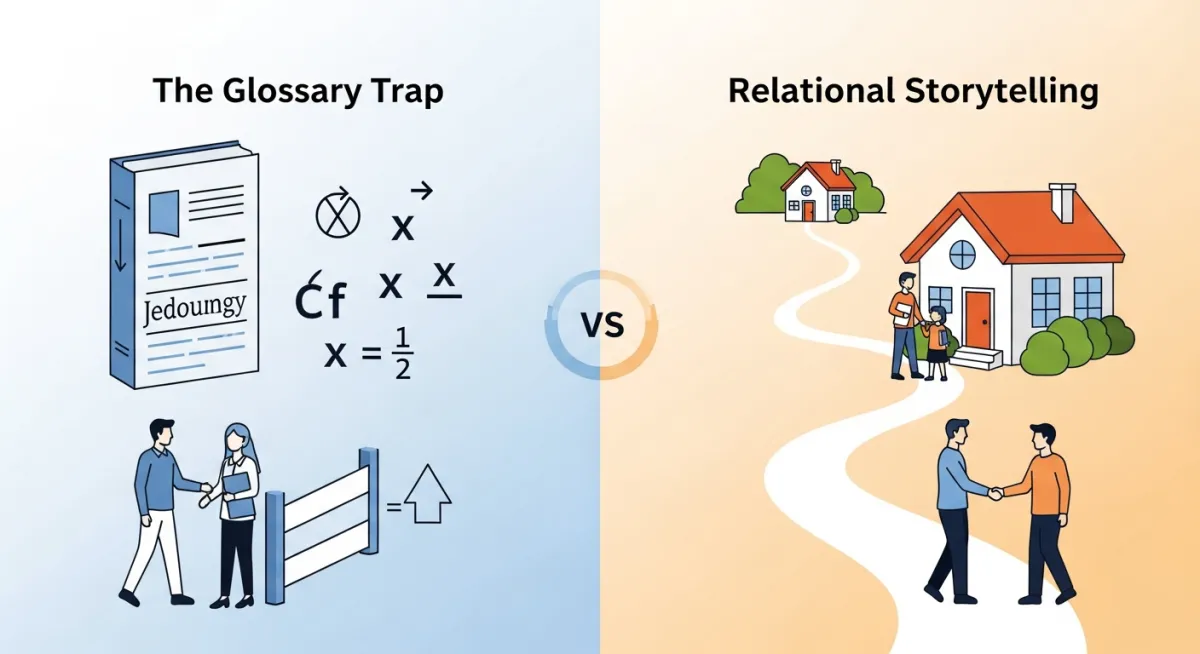

The "Glossary Trap" and the Failure of Traditional Financial Marketing

Moving away from the 'Glossary Trap' toward relational storytelling transforms your marketing from a cold transaction into a trusted partnership.

Search results are full of robotic explanations about interest rates and amortization periods. While these define the "what," they fail to address the "why." Clients don't want a dictionary; they want a partner to navigate the vulnerability of taking on significant debt. When you lead with jargon, you create distance. When you lead with empathy, you build authority.

Moving from Transactional Content to Relational Storytelling

Data builds credibility, but stories build relationships. When you frame home loans as a vehicle for personal growth rather than just a bank product, you transform the interaction from a transaction into a partnership. Focus on the client’s "why"—the family home, the retirement nest egg, or the transition to a new city.

Understanding the Emotional Burden of the Homebuying Journey

The average Canadian homebuyer carries immense weight—from down payment pressure to the fear of rising interest rates. Recognizing this emotional burden shows you understand the client. It helps build trust right away.

Social Proof: Why Clients Follow the Crowd Toward Specific Mortgage Options

People look to their peers to validate major financial choices. When you highlight successful client outcomes, you provide the social proof required to lower their guard and increase engagement with your mortgage options.

The Fear of Missing Out (FOMO) and Interest Rate Volatility

Fear of missing out on interest rates can stop people from making decisions. By reframing market fluctuations as manageable variables, you replace anxiety with empowered action. Educate your audience on why market timing is less important than long-term strategy.

Home-Equity Envy: Tapping into the Aspirational Nature of Real Estate Investments

Property is often seen as a status symbol. Tapping into the desire for long-term home equity growth can turn a dry conversation about debt into an inspiring vision of future wealth.

Reframing Technical Hurdles as Psychological Solutions

Changing technical mortgage problems into psychological solutions helps clients feel supported. It stops them from feeling overwhelmed. Whether discussing Loan to Value or the prime rate, your goal is to translate technicality into clarity.

Addressing the Stress Test: Turning a Barrier into a Safety Net

By dealing with the emotional stress of a high-ratio mortgage purchase involving default insurance, you can change the stress test into a safety tool. Position the test not as a "no," but as a professional assessment that ensures they don't overextend their Mortgage Payments.

Explaining Debt-to-Income Ratio Without the Math Headache

Shift the focus from the ratio itself to the concept of "financial breathing room." Explain that the Debt-to-Income Ratio is simply a way to protect their lifestyle from becoming a slave to their home mortgage.

The Psychology of Choice: Helping Clients Navigate Fixed-Rate vs. Variable-Rate Mortgages

A Variable-Rate Mortgage can be a smart tool. But it only works for people whose mindset fits its ups and downs. Compare this against a Fixed-Rate Mortgage to help clients align their product choice with their personal risk tolerance.

The Hero’s Journey: From High-Ratio Mortgage to Homeownership

The client is the hero, and you are the guide. By showing them how to navigate the application process, you help them overcome the hurdle of a high-ratio mortgage to achieve homeownership.

Case Studies in Resilience: Overcoming Credit Score Anxiety and Application Rejection

Sharing stories of resilience when facing financial hurdles builds immense trust and authority, especially when using an A lender vs. alternative options.

Positioning the Mortgage Professional as the Guide, Not the Hero

Being humble helps people connect. Emphasize that your role is to provide the map while they make the journey, ensuring they don't fall for predatory financial products.

Making Amortization Schedules Visual and Relatable

Use a Mortgage Payment Calculator to create visual timelines. When clients see how their amortization period affects interest costs, they are empowered to make faster payments.

The "Wealth Narrative": Reframing Debt Management as Equity Building

Teach clients that their mortgage is an investment, not just a monthly payment. Frame debt management as a system for wealth creation.

Using a Mortgage Payment Calculator to Reduce Financial Uncertainty

Tools reduce noise. When clients can model scenarios regarding closed mortgages or open-term mortgages, they gain confidence in their decision-making process.

Addressing the Imposter Syndrome of First-Time Buyers

Many buyers feel they "don't belong" in the financial markets. Your role is to normalize their journey and confirm their eligibility through financial statements.

Building Trust in an Era of High Interest Rates and Market Fluctuations

Consistency and transparency are your greatest assets. Ensure clients understand that market shifts do not invalidate their long-term financial strategy.

The Role of Transparency in the Disclosure and Application Process

Being completely open removes doubt. Clearly explain collateral charges and prepayment charges to ensure a smooth, informed experience.

The Educational Pillar: Demystifying CMHC and Default Insurance

Explain default insurance as a mechanism for access to capital, rather than just an additional cost.

The Wealth Pillar: Utilizing HELOCs and Leverage for Long-Term Strategy

Show how a Home Equity Line of Credit (or a line of credit) can be a strategic tool for financial flexibility and leveraged investing.

The Lifestyle Pillar: Connecting Property Values to Personal Freedom

Ultimately, link the asset to the dream. A home is not just a structure; it is the foundation for personal and real estate investment freedom.

Final Thoughts

Successful mortgage marketing requires moving beyond math to master the psychology of the homebuyer. By addressing the emotional weight of a purchase, reframing the stress test as a safety tool, and highlighting equity building via a Home Equity Line of Credit, you provide genuine value. Use storytelling to simplify the process and serve as a reliable guide in an unpredictable market. Shift your focus to the human experience, and you will find your authority growing naturally. For further reading, consult the Financial Consumer Agency of Canada to stay updated on federal rights regarding credit discrimination.